Why imagine a world beyond money?

In this episode, we explore more about the money-economy, and why it’s so important that we move away from that mistake.

In previous episodes here, we’ve explored the idea of a focus on value, rather than money, as an anchor for future change; and then set out to imagine a world beyond money. But why? What’s the value in doing this?

One of the core concerns of economics and the like is about management of resources, particularly at larger scale and over longer periods of time. Another core concern is about guidance of change, often across the entire scope of that economics. For these and other concerns, probably our most common concept at present is to describe everything in monetary terms: price, cost, budgets and the like. In business, the money – where it comes from, where it goes – is often almost the only thing we’d be expected to think about. Money as the main metric for everything; money as the main means for managing resources.

Yet how well does that actually work, to satisfy all of those needs?

In those previous episodes we saw that money doesn’t work well as ‘the metric for everything’, the sole measure of value: there are too many important things that get hidden from view if we focus only on money. So maybe the same might apply to the money-system itself, as a means for managing resources? Maybe there are some hidden assumptions there that we might need to bring to the surface?

In which case, let’s explore this with another practical experiment…

First, let’s imagine the key steps in the stereotypic human life-sequence – from child or teenager still living at home, to first leaving home, to moving in with a partner, to having kids, the kids at school, the kids themselves leaving home, and onward to retirement and old age.

(This experiment often works better if we make this personal: so imagine that this is you we’re describing here – your own history so far, and your expectations for the future.)

Given that, let’s apply that test of ‘What do you need?‘: what were, are or would be the resource-needs that you and others have, for each stage in that life-sequence?

For example, as a teenager, most of your needs would have been met by someone else – your parents, most usually. (Note we’re talking about needs here, not wants – the wants of a teenager are often limitless!)

So when you first leave home, what are your needs then? What are the changes? For most people, it’s probable that your needs would suddenly skyrocket: you’d need somewhere to live, the deposit for the rent, and the furniture and bedding and kitchenware and all the other sheer stuff that makes a household work.

What happens when first you move in with a partner? What are the changes at this stage? For most, it’s probable that your needs would plummet, as you not only gain economies of scale – two for the price of one, for a lot of things – but you probably have too much of everything left over from when you each lived on your own.

Keep walking through that life-sequence: what happens when babies start to arrive? When the children go to school? On and on through the whole of that sequence… And perhaps throw in a few periods of illness or unemployment along the way, just to add a bit more detail. What are your needs, at each stage?

Once you’ve explored that sequence, map it out as a simple graph, with age in years as the x-axis, and level of needs, from low to high, as the y-axis. (If you prefer, map the y-axis in terms of expenditure, of monetary outlay to satisfy those needs – in our money-based economics, it comes to much the same thing.)

My guess is that your graph will look something like this, with wild swings from one extreme to the other:

For the next part of the experiment, describe or imagine the actual or probable resource-availability for each stage in that same life-sequence – teenager, first leaving home, moving in with a partner, and so on. Again, perhaps add a few periods of illness or unemployment along the way, to make it a richer picture.

In our current money-economy, probably the simplest way to do this is to map it out in terms of monetary income – what pay or other income you have, at each stage. Model this as your own household-income, you as an individual, as a couple, as your own immediate family: keep others out of the picture at present.

Once you’ve explored that life-sequence in terms of likely resource-availability, map the result out in the same way as for the previous graph. Again use age-in-years as the x-axis, but this time, rather than resource-needs or expenditure as the y-axis, show resource-availability or income.

My guess is that this time your graph will look something like this:

Again, a lot of wild swings there, often from extreme to extreme.

For the final step in this exercise, compare resource-needs to resource-availability throughout that stereotypic life-sequence. The simplest way to do this is to put the two graphs together – a combined graph, with a red trend-line representing typical resource-needs at each point in the life-sequence, and a green trend-line representing typical resource-availability at the same points in that sequence. Hence if we combine those two example graphs above, what we’d get is something like this:

Yeah – it’s an almost perfect mismatch. Whenever we least need resources, we’re most likely to have them; and whenever we most need resources, we’re least likely to have them. To put it another way, what this shows us is that the natural tendency – the ‘gravity’ – of our entire money-based economy is to move resources to wherever they’re least needed.

As a means of managing shared resources, our money-based economics is not merely a poor system – it’s arguably the worst system that we could possibly devise. And yet that’s the inherent nature of the system that we live in at present, day after day, year after year, for all of our lives.

Ouch…

To make our economics at least seem to sort-of work, we need to counter that natural-gravity of the system. Hence the huge infrastructure of banking, insurance, tax, pensions and more, to try to move resources around to when and where they’re actually needed. Hence also money itself, as a sort-of standardised means to measure, monitor and manage that time-shifting of resource-needs and resource-availability. Yet that infrastructure is colossally expensive: put all together, it already accounts for around half of all ‘economic-effort’, and still rising fast. All of it dangerously fragile, wide-open to all manner of misuses. And all of it is colossally inefficient, given that all of its effort is pushing against the natural-gravity of the entire system.

In short, as a means for managing our shared resources, our current money-based economics doesn’t work. Not well. Not for most people. Probably not for anyone, in the longer run.

Ouch…

We definitely need to do better than this.

Which is why we need to imagine a world beyond money.

The next question, of course, is how.

We’ve seen in the previous episodes that we can imagine a world beyond money.

We’ve seen here why we’d need a world beyond money.

The next question is how we could build a world without money.

Which, for most of us, might seem an impossible task. Way out of scope for anything we might do.

But actually, no: we can do it.

Because money isn’t actually the real problem here. Nor is the money-system, or anything built upon it.

It’s not even anyone’s fault: there’s no evil ‘Them’ to blame here.

It’s just us. All of us, doing what we do. But doing what we do, in context of a bunch of unquestioned myths about ‘how the world really works’.

The one most useful thing right now that we can do about this is to worry less about what’s happening on the surface, and instead start to explore the hidden assumptions behind those myths.

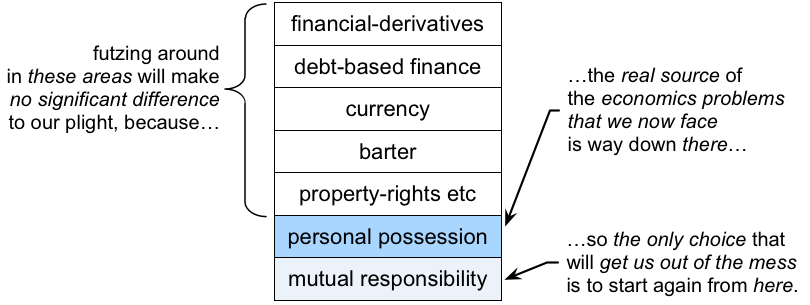

The catch, as we’ve seen in previous episodes here, is that the myths we most need to explore and resolve are a lot further down than we might expect:

As in the graphic just above, the key emphasis around concepts of ownership – in particular, the crucial distinctions between possession, versus responsibility or stewardship. For example, it doesn’t take much exploration to recognise that there’s no way to make a possession-based economics sustainable in the longer-term – whereas a responsibility-based economics can be made sustainable indefinitely. And again, getting clear on what works and what doesn’t at larger scales can provide real value for how we build for our organisations and more.

But where do we start? How do we find the ‘How‘?

One worthwhile place, perhaps, is with what we’d explored in the previous episodes: that concept of value, and that process of replacing every monetary transaction with the simple question of “What do you need?”. And then apply all of that, to look at ‘the economy’ as a whole.

So let’s do that, in the next few episodes here: start to put all of this theory-type stuff into real-world practice.

(Note: This episode has been adapted from my post ‘RBPEA: Why imagine a world beyond money?’, first published on the Tetradian weblog in July 2019..)

Just brilliant Tom, used this same thinking when we addressed product development to meet customer life stage. It is therefore not a clever idea to produce a mailshot to all customers for funeral insurance cover if 40% of your client base is between the ages of 25-35. What they probably need is mortgage cover, education savings schemes for children, etc,..

By mapping your client base to the graphs you produced above your marketing mailshot would have more impact if approached from client life stage. The mentioned funeral cover would have more impact on the 60-90 age group in your graph. The savings on wasted marketing can be utilised to enhance client offerings where required.